In what looks like a tentative bright point for the aerospace sector, Rolls Royce reported profits of £307 million for the first half of 2021 on 5th August, as demand slowly returns to an aviation sector decimated by COVID-19.

A take-off after a prolonged emergency landing?

It comes at a pivotal moment. Rolls Royce stocks are trading at less than a third of their 2018 level. The aerospace manufacturer reported losses of $4 billion in 2020, which significantly put a dent in their valuation, accelerated by a dilution exercise of shares in a fight to save the company’s long-term prospects. These profit reports indicate that bet is beginning to pay off.

Rolls Royce return to making headways in aviation

They now move up the rankings in a club of manufacturers and airliners that have seen significant devaluation since the onset of the pandemic. Bombardier may never recover from their losses since 2018, a result of early spiralling costs compounded by the pandemic. Airbus, meanwhile, have seen relatively unabated growth, with share prices more than doubling from their floor from May 2020. Already it seems, there are bigger losers than others in this structural shock to aviation.

Though it is unlikely that any aviation company will be cheering further losses amongst their competitors, in what is an industry-wide inflection point for the aviation industry. The sector has been the golden child of the 21st Century, with affordable travel mushrooming, and the growth of professional service sectors setting a path for the highly profitable business travel sub-sector. In 2019, airlines generated $838 billion in turnover, almost triple its 2003 revenue of $322 billion. Its 2020 revenue of $372 billion seemingly brings the sector back to square one. They also undid more than five years’ worth of profits with a $126 billion loss through COVID.

Travel back on trend, but gaps to be plugged

But hope is on the horizon for the battered travel sector. Passenger numbers are tentatively rebounding – in the States, the Transport Security Administration (TSA) counted 67 million passengers through US airports in July, closing in on the pre-COVID 89 million from July 2019, and well ahead of the 23 million from the same time last year. Aircraft orders are recovering more speculatively; Airbus are hoping for a big H2 of 2021 following a 10-year low of 383 orders in 2020, and a slow H1 2021 of 167 orders. Most of these, unsurprisingly, are on short haul, single-aisle planes.

Closing the gap: Weekly TSA Checkpoint Travel Numbers (millions)

Source: TSA

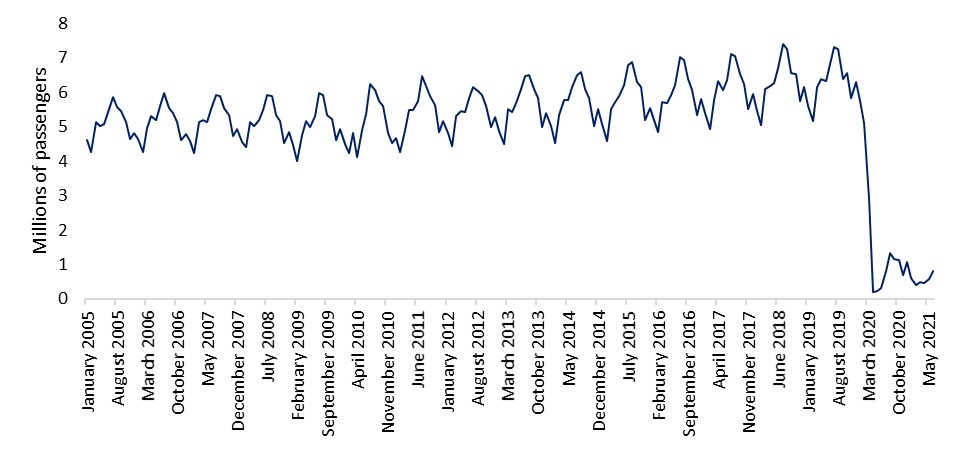

Unfortunately, air travel now appears stuck at a halfway house, with a weekly shortfall of between four and seven million passengers in the US. It is this final gap that will be hardest to close. The resounding success of vaccine rollout across the Western world contrasts with developing countries; the UK has fully vaccinated more than 58% of its population, India has fully vaccinated 8%. This shortfall will inevitably present as a problem for international travel, the US maintains strict travel restrictions on nearly every country. Likewise, the UK’s traffic light system has nearly obliterated its international tourism industry: international travel through Heathrow in H1 2021 was less than 10% the H1 2019 rate. These rates are expected to recover more quickly than other travel indicators – namely business – but variants test even the most bullish forecaster’s confidence about when.

International air passengers travelling through Heathrow, January 2005 – June 2021

Source: Heathrow Airport

Until then, the shares of Rolls Royce, Bombardier, EasyJet et. al will likely continue to underperform their potential. But as consistent, seemingly irreversible reopening continues across the developed world, it is also likely that they have reached their floor. Expect a long, uphill battle; the International Air Transport Association (IATA) project that revenue and passenger numbers will return to pre-covid levels by 2023.

Business travel will be more tricky – firms have to some extent grown happy with their Zoom, Skype and Teams arrangements since March 2020, particularly given how it effects their bottom line. As a result, McKinsey & Co predict business travel will only recover to 80 percent of pre-covid levels by 2024. However, the rise in corporate bookings – particularly domestic – as lockdowns lift in more vaccine-advanced countries, should act as a heartening sign for those dependent on the return of travel commerce.

New obstacles for a new world

Of course, aerospace returns to a new world, a world that is one year further down the line of climate change, as well as the changing consumer and business preferences outlined earlier. Its long-term survival depends on adapting to the needs of the climate, primarily through the rollout of sustainable fuel, in order to cut is 2.5% share of global Co2 emissions. After the pounding it continues to take from COVID, the aviation sector can scarcely afford to put a foot wrong come the next crisis.

Of course, aerospace returns to a new world, a world that is one year further down the line of climate change, as well as the changing consumer and business preferences outlined earlier. Its long-term survival depends on adapting to the needs of the climate, primarily through the rollout of sustainable fuel, in order to cut is 2.5% share of global Co2 emissions. After the pounding it continues to take from COVID, the aviation sector can scarcely afford to put a foot wrong come the next crisis.

To bet on the airline industry in the long term is to bet that consumer habits will change once more, as well as those of businesses. That comes before factoring in how national governments and the industry respond to climate change. In the medium term, it is a bet that is likely to pay off. And while the horizon is further with the benefit of altitude, myriad uncertainties mean the future of aviation remains hazy.